Strong winds in Estonia and across the Baltics helped pull power prices down sharply compared to November

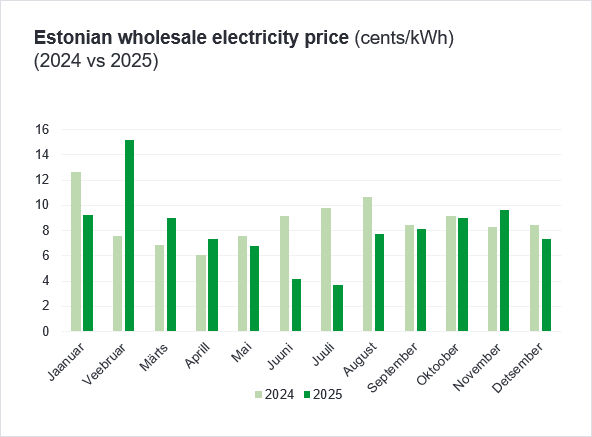

December brought mild “Christmas weather”, but without the strong snow and cold that we have often seen in recent winters. The average price fell by almost a quarter versus November, down to 7.37 cents per kilowatt-hour. Compared to December last year (8.43 cents per kilowatt-hour), the average price was also lower (-13%), as 65% of Estlink 2 was unavailable last year.

Compared to Latvia and Lithuania, Estonian power prices were about 12% lower – Latvia and Lithuania both averaged at 8.40 cents per kilowatt-hour. The explanation is simple and still relevant today: as the Estonia–Latvia interconnectors remain heavily limited (almost cut in half), a large part of cheap Finnish electricity remains within Estonia, which keeps prices elsewhere higher than they otherwise would be and consequently, prices cheap in Estonia.

Estonian prices in December were mainly pushed down by very strong wind production in the region together with cheap Finnish imports. Within the entire December, Estonia imported at full Estlink 2 capacity from Finland almost 72% of the month (at 1016MW). However, in all of December, Estonia imported at least 900MW, meaning that the entire month Estonia was importing almost at full capacity from Finland. Nevertheless, Estonia averaged at almost twice as high prices for December as Finland’s average price for the month remained at 3.6 cents per kilowatt-hour. Wind generation covered slightly over a fifth of total December demand, imports covered a significant 49% (which is the largest number seen in December in the past 10 years), and fossil assets brought in another fifth.

Year 2025 in Estonia: fossil assets lost even more ground in everyday consumption, solar and wind picked up significantly

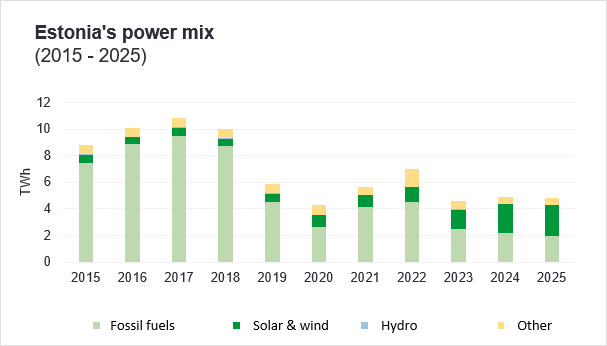

The average electricity price in Estonia for 2025 ended at 8.09 cents per kilowatt-hour. That is almost 0.6 cents per kilowatt-hour lower than last year, and close to 1 cents per kilowatt-hour lower than 2023. Since 2020, the Estonian price zone has seen major ups and downs: the 2022 energy crisis, interruptions and limits on the Finland–Baltics connections, the impact of balancing costs, rising CO₂ prices, and a volatile gas market. Even with all this, prices have stayed relatively stable overall – the three-year average is 8.63 cents per kilowatt-hour. At the same time, today’s prices are very different from the pre-crisis period: in 2020, the average power price was only 3.4 cents per kilowatt-hour.

While prices have remained stable for the past three years, the power mix has slowly, but steadily changed. In 2023, around 30% of local demand was covered by fossil-based assets – a number that has now decreased down to 24%. In that same period, the share of wind and solar from an annual perspective has risen to slightly over a third from 20% in 2023. The importance of imports has remained relatively stable – this year, almost 40% of total consumption was covered by imports, despite Estlink 2 being offline in the first part of the year.

Although wind and solar have continuously grabbed a larger share of production, fossil-based assets have lost their share significantly: while in 2017 fossil-based generation remained at close 9.5 TWh of production and Estonia was a net exporter, this number has now fallen close to five times to 1.9 TWh. This is a result of market dynamics: cheap marginal cost assets are grabbing their market share, coupled with cheap imports from Finland, therefore yielding a lower prices which in turn causes a situation where it is not profitable for fossil assets to produce in the markets.

In total, Estonia generated close to 4.8 TWh of electricity, down by over a half from 2017 where the total production ended at slightly over 10 TWh. The rest of the electricity was imported – most from Sweden, but also from Latvia and Lithuania, but also from Sweden and Poland through the interconnections that Lithuania has to the rest of Europe.

What could happen next month and next year?

In the next five years, more risks are approaching against the recent rapid renewable buildout. A key reason for this is price cannibalization, which weakens the business case for new wind and solar projects. The logic is straightforward: when solar output is high, many panels generate at the same time, pushing prices down so much that producers earn very little (sometimes close to zero, or even negative prices). The same happens during strong wind periods. This can push project payback periods from 5–10 years to 20–30 years, which makes financing much harder.

Because of this, the number of extremely cheap hours (for example, prices below 1 cent per kilowatt-hour) may not keep rising as fast as it has over the past five years. Instead, we may gradually see prices becoming more even. Battery buildout should help smooth both wholesale and balancing prices, through simple arbitrage: charging when prices are low and discharging when prices are high or regulating markets up or down, when balancing is needed. This reduces volatility and helps stabilize the system. Even with strong renewables in Lithuania and the Baltics, more dispatchable capacity is still needed to keep prices stable for consumers. One option could be low marginal cost production plants that can participate in both balancing and day-ahead markets.

Looking at next month, conditions may be similar to December. Prices will depend heavily on temperature, import availability from the Nordics, and especially on low-cost wind production. If imports are limited and wind is weak, we could see a month like February last year, when prices averaged 15.2 cents per kilowatt-hour and the market was often set by expensive units such as Estonian oil shale or older gas plants. If wind is very strong and imports are available, lower prices can be expected.

Karl Joosep Randveer, Energy Trading Analyst at Enefit

The market overview has been compiled by Enefit according to the best current knowledge. The information provided is based on public information. The market overview is presented as informative material and not as a promise, proposal or official forecast by Enefit. Due to rapid changes in the regulation of the electricity market, the market overview or the information contained in it is not final and may not correspond to future situations. Enefit is not liable for any costs or damages that may arise in connection with the use of the information provided.