Energy Market Overview: Strong Links with Finland Secured Estonia the Lowest Power Price in the Baltics

- Estonian power prices rose in November due to colder weather and higher heating demand. Thanks to strong connections with Finland, Estonia remained the most affordable market in the Baltics.

- Lower regional wind output, the end of the solar season, and maintenance on key interconnectors and gas units increased reliance on fossil generation, pushing prices upward.

- Imports from Finland covered more than half of Estonia’s demand. Estlink cables operated near full capacity for much of the month, bringing cheaper Nordic electricity to the Baltic market.

- Looking ahead to December, prices will depend mainly on winter weather and gas and CO₂ costs: cold, calm periods will keep prices high, while windier and wetter conditions could bring relief.

November Market Dynamics

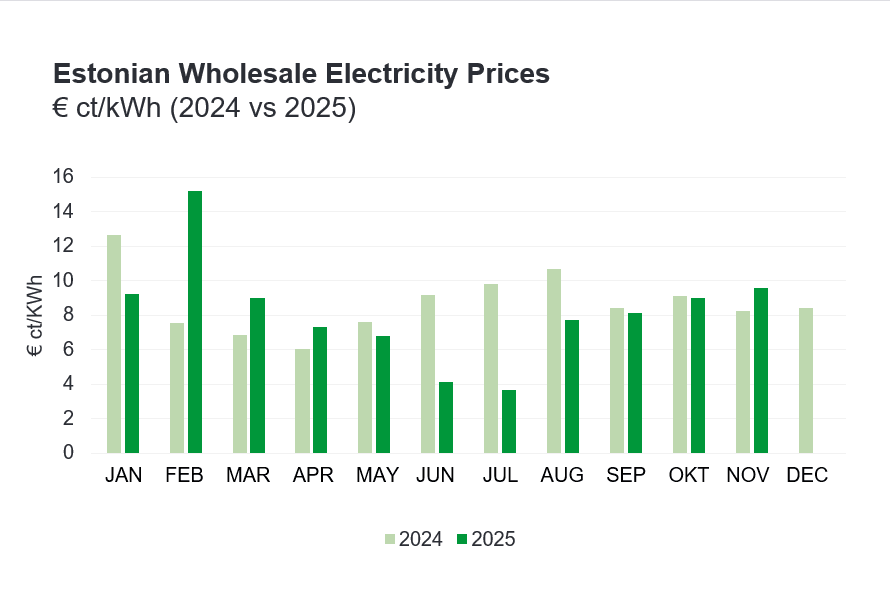

November brought colder weather, higher heating demand, and a tighter power balance. Average temperatures fell, nights lengthened, and daylight hours shortened. The main price drivers were regional wind generation, Latvian-Lithuanian gas and hydro output, Estonian oil shale, and Nordic imports. Compared to Latvia and Lithuania, Estonia remained the cheapest Baltic market thanks to better access to Nordic energy via Finland. However, transmission capacity between Estonia and Latvia was cut by more than half due to maintenance. As a result, Estonia’s average price reached 9.59 cents/kWh, up 7% from October and nearly 16% higher than last November.

Production Dynamics Shaped Prices

Wind generation—typically a key price-suppressing factor—fell by about 12.5% month-on-month and was roughly 25% lower year-on-year. With weaker wind, growing demand was met less by low-cost renewables and more by fossil-fuel plants, particularly Estonian oil shale and Latvian-Lithuanian gas units with higher production costs. This pushed prices up, with about 20% of November hours exceeding 15 cents/kWh.

In summer, weak wind is often offset by strong solar output, which keeps fossil plants out of the market. In November, however, the solar season was effectively over: while solar covered up to 25% of Baltic demand in June, its share dropped to just 2.2% in November, leaving no meaningful price-dampening effect.

Local wind covered 13% of Estonia’s demand, down sharply from 24% last year. In winter, when the alternative to wind is expensive fossil generation, a steep drop in wind output almost inevitably means higher prices. System flexibility was further reduced by maintenance on a key Lithuanian gas unit, which limited the ability to respond during peak hours and forced more costly plants into the mix. On the positive side, Latvian hydropower output increased significantly— twice as high as in October and about 30% above the five-year average.

Imports from Finland Were Crucial

Net imports accounted for slightly more than half of Estonia’s demand in November. Estlink 1 and 2 ran at full capacity (1,016 MW) for nearly two-thirds of all hours, meaning cheaper Finnish electricity flowed into the market most of the time. For context, Finland’s average price was 4.79 cents/kWh, roughly half of Estonia’s, supported by cheaper nuclear and wind power and Swedish and Norwegian hydro imports.

Price Volatility and Storage Opportunities

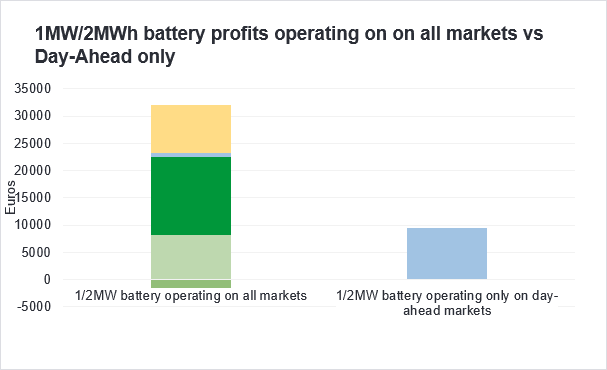

Intraday price swings remained strong in November, though less pronounced than in October. These fluctuations created attractive opportunities for storage solutions: a 1 MW / 2 MWh battery could have earned close to €9,500 on the Baltic day-ahead market by charging during low-price hours and selling during peak hours. If the same battery had participated across all market segments (aFRR, mFRR, FCR, intraday, and day-ahead), potential revenue could have reached €30,000. While this assumes ideal operating conditions, it underscores the importance of flexibility for profitability.

Outlook for December

Prices will be driven mainly by weather—both temperature and wind. On cold, calm days with high heating demand, prices are likely to stay in the 10–15 cents/kWh range and may often spike above 20 cents/kWh. If typical winter wind conditions return, low-cost wind power from Lithuania, Estonia, and the Nordics could reduce reliance on expensive fossil generation and bring prices down. Continued growth in Latvian hydropower could also help shave peak-hour prices, as flexible hydro plants ramp up during the most expensive hours.

Another key factor will be gas prices: a sharp increase would quickly feed through to electricity prices and consumer bills. For now, gas remains very low—around €30/MWh —helping keep gas-fired generation costs down in the Baltics. However, this positive effect is partly offset by rising EUA CO₂ prices, which increase the cost of carbon-intensive generation.

Karl Joosep Randveer, Energy Trading Analyst at Eesti Energia

The market overview has been compiled by Eesti Energia according to the best current knowledge. The information provided is based on public information. The market overview is presented as informative material and not as a promise, proposal or official forecast by Eesti Energia. Due to rapid changes in the regulation of the electricity market, the market overview or the information contained in it is not final and may not correspond to future situations. Eesti Energia is not liable for any costs or damages that may arise in connection with the use of the information provided.